It is difficult to understand what was truly achieved at COP 26. After pre-weeks of media to COP 26 and then the concerted media campaign during the week of COP 26 how do we sort the wheat from the chaff or the greenwashing from the truth.

Fundamentally, there is still a long, long way to go. COP 26 was not the breakthrough that was needed. Both the public and private sectors did not step up and demonstrate the urgency that was needed.

Here are my 10 key thoughts:

1. COP 26 was more than blah, blah, blah, as Greta Thunberg said; but, it fell far short of what was needed. It was inevitable that we would fall short of 1.5 degrees Celsius, the question was really how far? The best guess seems to be that the commitments added up to about a 0.3 degree Celsius improvement moving our current likely outcome tracking from +2.7 Celsius warming at 2050 to 2.4 degrees (per Climate Analytics Tracker or CAT). In Climate Actions latest publication, they noted that not only do the commitments fall short of the +1.5C target of the Paris Climate Agreement, there is no single country that has put short term policies in place to put itself on track to its net zero target.

2. Out of Glasgow, there is recognition that this push to improve commitments cannot just happen every 5 years. This is a good move. They are now asking countries to each year look at ratcheting up their targets and actions. For most countries, setting 2030 targets rather than earlier targets is also a way to delay the need to address the problem to the next leadership group whether in the political or private sector arena. Given that the carbon emissions problem is a cumulative problem there should be a further goal of each country committing to a set of annual activities and targets; and, couple this with ‘naming and shaming’ of those that fall short. Ramping up public pressure is fundamental to proper progress.

3. COP 26 recognised that it is vital to solve the biodiversity issue as part of the climate problem even though it has a set of other issues. The reduction of deforestation pledge by 118 countries by 2030 is a start in the right direction. This should be enacted much faster. Nine more years of deforestation is a problem. The devil will be in the detail of the agreement; including, the addressing of illegal logging and the need for reforestation. The three regions of particular concern are the Amazon, the rainforests of Indonesia and the Congo Basin.

4. The announcement of GFANZ (Glasgow Financial Alliance for Net Zer0) having 450 organisations that manage $130tn of private wealth saying they will participate in the financing of the climate challenges is a good start. Mark Carney has made good progress to pull this together. The cynic would say that if there was $100tn of investment opportunities (the size of the climate challenge) that will add 2% per annum of economic growth and they were presented as good investment opportunities who wouldn’t want to be part of the club. The key question is in reality will this result in large scale material changes in investment allocations and what will it also take to make this happen in terms of reporting, policy and regulatory changes, carbon tax, last mile of risk security, etc. The reality is this is a step in the right direction; but, there is a long way to go.

5. COP 26 forgot the oceans which is the biggest carbon sink. Where is the equivalent pledge to deforestation for the Oceans. What never seems to be included in the Net Zero discussion is that the goals required do not consider any indirect impacts of carbon emissions (including other GHCs) that are in carbon sinks on land and in the oceans. Only a very small percentage of GHCs are in the air vs. absorbed in the land and oceans and their biodiversity. The melting of ice and permafrost, the warming and acidification of oceans, and the equivalent of ocean deforestation from over fishing are likely to release GHC’s into the air. There are also other indirect sources of warming that have also not been considered.

6. COP 26 needs to get away from the sole narrative of clean energy and focus on the reality of a practical transition to clean energy. The coal and methane pledges are helpful but are really subsets of existing pledges that should already have been made or identified in terms of carbon emissions reduction to meet the 2030 targets that each country committed to. Countries should be solving not just the optimal future state of energy provision but also the economics of transition vs. the related cumulative impact of emissions. Optimal transition will require continued fossil fuel extractions (hopefully focused on the least climate damaging approach), being realistic on the ideal role of nuclear power and other credible low emission sources, and ensuring there aren’t economically disruptive shortages on the way. Governments have a big role to play in this in terms of creating the right economics of alternative energies (through carbon taxes, subsidies, other policies) and their own commitments to ensuring the appropriate energy grids are in place to maintain steady supply.

7. We still need more discussion on adaptation not just carbon emissions reductions. It has been good to hear that there are now some more realistic discussions on climate that are appropriately also talking about adaptation. The short to medium term economic benefits of dealing with climate change come from adaptation while the longer term benefits are from reaching Net Zero. Developing and underdeveloped countries are primarily concerned about adaptation to deal with the economic consequences of extreme weather. The first things they need are economic assistance to social and economic development to help deal with the ravages of droughts, increased heat, floods, etc. resulting from climate change. These include factors such as access to water, crops which are more resistant to the new climate reality they are facing, and access to 24/7 low cost energy ( and ideally low emission energy) for development. Given that a significant proportion of those in extreme poverty are subsistence farmers specific targeting of assistance programs will be essential.

8. Carbon tax hesitancy. It could be argued that the one thing that would indicate how governments are taking climate change seriously would be the agreement of a global carbon tax, or cap and trade, system. This also includes dealing with addressing the issue of heavy subsidies on fossil fuels in many countries including the United States. The shifting of the relative economics of alternative energies is vital to accelerating the investment in and adoption of new energy consumption habits. There has been no apparent progress on a global carbon tax program.

9. Global North and Global South was not properly recognised in COP 26. In the climate conferences, the Global North refers to developed countries; and the Global South are the developing and underdeveloped countries. The Global North completely dominates both the emission of GHCs and the use of fossil fuels. The global south has a small fraction of per capita consumption of energy; although, they do contain the large and growing proportions of the population. These countries have primary priorities on social and economic development which involves growth in energy consumption before achieving net zero is even considered. Very different programs of climate action should be targeted for common clusters of countries; rather than the chasing of universal agreement on a common set of actions. Why do we keep chasing all countries to sign up to the same agreements?

10. The increased level of stakeholder activism and engagement needed to drive change was not properly incorporated into the conference. There needs to be a much higher level of activism by stakeholders to drive change and hold politicians and private sector leaders accountable. The activism needs to include the public voting out of politicians, the boycotting of companies and withdrawal of funds from irresponsible companies by investors and insurers. In the same way that there needs to be activism there also needs to be proactive engagement of stakeholders in changing their own behaviours with respect to both the shift to Net Zero and addressing adaptation requirements. This means that every individual, town, municipality, city, province, country and region, as well as every other organisation in any form, has the simple requirement of acting themselves. This was completely missed at COP 26 as they tried to focus on newsworthy narratives vs. practical solutions.

As an optimist, I do think that we have the wherewithal to succeed. To do this we need to face the truth, deal with reality, and stop greenwashing problems and challenges. Transparency is essential, programs must be put on the ground and managed to time, results must be monitored, and actions must be taken against shortcomings.

“If we are to have peace on earth, our loyalties must become ecumenical rather than sectional. Our loyalties must transcend our race, our tribe, our class, and our nation; and this means we must develop a world perspective.” Martin Luther King Jr.

Hans Rosling said how can you solve major challenges if you don’t understand the facts. He was a Professor of International Health at the Karolinska Institute and Founder and Chairman of Gapminder Foundation. As a well known and influential speaker on global issues, he used to systematically ask 10 questions to his audience about the state of the world. To his dismay he found that no matter the intelligence of his audience their true understanding of the world fell well short of being even adequate. In fact, their overall scores were worse than what a chimpanzee would score with random picks. His final book, “Factfulness – Ten reasons we are wrong about the world – and why things are better than you think”, dealt specifically with this issue. He was on a mission to save people from their preconceived ideas.

This is the tenth and last blog of this World View series. This series came about as I felt that it was vital to be up to date with the current state of the world across a number of dimensions and develop an integrated world view of where we are and where need to be going. This series was the result of over 18 months of extensive research across a broad range of subjects learning from the works of Nobel prize winners, professors, researchers and well respected individuals. It also involved analysing different databases, reading research and using the power of the web to capture information, understanding and alternative perspectives. I have tried to look at our world in an integrated way and explore a range of perspectives and not just confirm cognitive biases I already had. It is safe to say that my view of where we are and what we need to do going forward at the global level is different from my initial thoughts. What is unchanged is that I remain optimistic. To be an effective leader going forward I believe having a grounded world view is essential. Building successful sustainable businesses cannot be done in isolation anymore.

In the first blog, I laid out what I thought were the three big global challenges that needed to be addressed. Although being more tightly defined, not surprisingly they were consistent with the UN Sustainable Development Goals and the World Economic Forum Global Risk Report. The three challenges as I defined them were:

Decarbonisation and Biodiversity Regeneration

Inclusivity and Fairness

Digital Privacy and Collective Truth

In the second blog, I analysed the components of successful societies. The third blog, set the scene for thinking about the challenges going forward in the context of what should be the social contract for citizens of a society. The next three blogs covered off different aspects of delivering against the social contract – democracy and the role of government, the market economy and capitalism, and the nine waves of technology innovation. Blogs 7 to 9 each explored in more detail one of the three challenges, including thoughts on how to solve them.

This tenth blog explores the keys to unblocking one of the most critical barrier to success, urgency and alignment. It is not a case of not understanding the challenges, shortcomings in our scientific knowledge, a lack of potential solutions; rather it is a lack of urgency and alignment that will make us fall short. And, don’t forget the consequences are immense! Together the challenges are solved by underpinning them with policies, incentives and appropriate stakeholder pressure provided on a timely basis. Given where we are, we know that the current governmental policies and the outcomes of our market economies and capitalism have been inadequate, and therefore, need to change. As Albert Einstein said, “The definition of insanity, is doing the same thing over and over again, but expecting a different result”.

Getting the right balance of incentives, carrots and sticks, across participants that need to change is the biggest challenge. The shaping of them must take place from the supra-national level, to national/regional/local governments, to the private sector, the third sector and to the public itself.

In the last few weeks, we have seen some critical indicators that we are making progress on this topic of urgency at the governmental level. In late April, Germany’s Federal Constitutional Court made a judgement on Germany’s 2019 Climate law which set as a target to cut 2030 carbon emissions by 55% from the level of 1990 and emit no net greenhouse gases by 2050. The Court ruled that the younger and future generations are entitled to “fundamental rights to a human future” and the current legislation results in a “radical burden” post 2030 on future generations that would drastically reduce their freedoms. The government now wants to lift the 2030 reduction target to 65%, and to bring forward the net carbon-neutral date to 2045. In a similar vein, in 2019 the Supreme Court of the Netherlands ordered the government to substantially increase its ambition after it watered down its carbon reduction target.

In Asia, there has been increasing legislation focused on digital censorship, including fake news, coming from a number of countries including Singapore, Malaysia, India and most recently Indonesia. Although, the focus includes dealing with the critical issues of national security, disturbance of public order and the conduct of elections; it can be said that much of the legislation is overreaching.

In the private sector, there is also progress. In a landmark climate case in late May 2021, the Dutch court ordered Shell to reduce its carbon emissions by 45% by 2030 from 2019 levels. This is in comparison to their current targets of 20% by 2030. In the same week, a small activist hedgefund, Engine No. 1, managed to replace two existing board members at Exxon with its own candidates to drive the company towards a greener strategy; and, Chevron shareholders rebelled against the Company Board by voting 61% in favour of forcing the group to cut its carbon emissions. Investors are increasingly taking these challenges seriously.

The cornerstone for making this happen is at the country level where government policies, taxes and incentives set the tone for the kind of society that needs to be built. They need to raise expectations for the private sector, and more diligently think about the social contract which they have with their citizens.

Supporting this are supra-national pressures to get all countries on board with the overall goals of fighting climate change and environmental degradation, and inequality. The UN Climate Change Conference in November 2021, COP26, will be a critical indicator of the level and urgency of ambition to tackle climate change at both the governmental level and by the private sector. There is also the 76th Session of the UN General Assembly in September 2021 which will be looking at the progress against the 2030 Sustainable Development Goals. In addition, ongoing pressure needs to be coming from the G7 and G20 conferences.

In addition, it is the involvement of financial markets, investors and asset managers that control the flow of funds to and from different sectors. The broad pressure points are coming from central banks, organisations such as Climate 100+ and ESG reporting requirements. Momentum is growing; however, the rate of change of aligning investment and financing decisions is too slow and the pressure for faster progress by the companies they are investing in is too light.

As long as boards and executive management are driven by short term strategies, thinking and incentives, change will be too slow. In large US corporates, changing the momentum from a continuously growing level of CEO compensation, from 30-40 times average worker compensation in the 1980’s to the current day level of 300-400 times, based on short term corporate performance to more challenging longterm performance with clear and ambitious impact goals is not in the self interest of these leaders. Boards must be willing to rapidly align the structure of compensation with long term sustainability. The Boards must be motivated to do this by the investors and asset managers; and where appropriate or needed by governmental policies, taxes and incentives. If leaders don’t adopt the need and urgency then nothing will happen. This is both a question of ensuring they are aligned with the priorities and they are leading with the right time horizons.

Finally, there are the citizens, who are also employees and customers, who need to use their voice and actions to drive change and must also change themselves. To do this they need transparency on the environmental and social behaviour of the company that is captured within the ESG reporting requirements. As noted earlier, both the court judgements and the shareholder actions were all triggered by stakeholder activism. More than ever stakeholders (employees, consumers, public, investors, etc.) are increasingly powerful voices that are requiring changes to corporate behaviour and a fundamental shift to responsible capitalism.

If you look at the private sector challenges, at its simplest level there are three dimensions to getting the incentives right and driving impact. Firstly, rewarding value and impact creators. Too much of our economy overly rewards value extractors, including profiting from trading and financial engineering, which adds little to the economy and nothing towards addressing these challenges. The question is, are you adding value and moving towards meeting the outcomes required by the challenges, or are you not contributing or falling short of the outcomes required. For any company or organization, if you have no measurable and relevant impact goals you should be seen as a value detractor regardless of what you are doing. Value creators should benefit in terms of governmental policies, tax levels and incentives in comparison to value detractors. Mariana Mazzucato, a leading economic thinker, has written a seminal book on this topic, “The Value of Everything – Making and Taking in the Global Economy”

Secondly, ensuring a proper balance of priorities across the short, medium and long term horizons. The challenges of climate change, biodiversity and inequality cannot be solved and be properly addressed in the short or medium term; however, investment in factors that have vital long term outcomes are required now. Achieving Net Zero for most companies and all countries will take more than 10 years; but, investment almost certainly needs to start now. Longterm investment behaviour should be rewarded vs. short term profit taking and extractive behaviour. Once again, policies, taxes and incentives are needed to assist in biasing investment returns towards impact focused investments.

Thirdly, addressing the challenges with the right urgency. This defines whether organisations own goals are in line with the timing of the needed/agreed collective achievement of the challenges.

To create urgency and alignment in incentives there are a few key principles. Firstly, the goals and related incentives need to be as simple as possible. Incentives must cover both value creation and impact in a balanced way. Secondly, the goals need to be clear, transparent, timely, measurable and auditable. Thirdly, programs and incentives must be adjustable to new and preferable technological solutions. Although overall long term targets are clear, interim targets and the set of actions to achieve them are not. Finally, incentive design must understand the heavy human bias towards focusing on easier short term goals and rewards vs. not comprising long term targets. It is a natural inclination to back end load change which often is beyond the work horizon of the existing leadership team. Early investment and impact gains are essential for success.

At the governmental level, it is vital that they set the tone in terms of level of ambition, timing and responsibilities. As I often say, uncertainty is the enemy of progress. Clear forward looking and stable policies, taxes and incentives will accelerate the commitment of investment by the private sector. These programs need to create alignment of the private sector with the goals and urgency of them; bias scale investment to meet these challenges; secure government financing to meet their own commitments; and, ensure the right research, development and innovation is happening to solve challenges where no economic solution currently exists.

Rightly so, there are concerns about overbearing and overly complex involvement of governments. However, it is also important to note that pure capitalism does not have a track record of solving these types of problems without the right involvement of governments. Policies, regulations, legislation, taxes and incentives need to set the direction towards outcomes and define the urgency; but not, specify the exact set of solutions. Marianne Mazzucato has defined this as “mission oriented” governmental programs. These activities should be designed to unleash the market power, speed and innovation capacity of the private sector to be the major contributor to the solution of these challenges.

In the second week June 2021, the senate broke their partisanship and agreed a mission oriented spending bill, the US Innovation and Competition Act, of a quarter of a trillion dollars focused on key technology sectors. This was achieved by defining it very much as a way the US can strengthen their competitive and adversarial position with China in key sectors. China has successfully had mission oriented programs to achieve leadership in specific technology sectors, including areas such as solar and electric cars.

So much can be achieved by just putting these frameworks in place, and then allowing innovation, financing and entrepreneurial energy to drive change towards the goals in the most effective way.

Without solving alignment and the creation of appropriate incentives using both carrots and sticks, it is highly unlikely that these challenges can be met on a timely basis.

I hope this series has been insightful to help you build your own World View. In this rapidly changing world, politically, economically and technologically staying abreast of where we are and what is possible is vital for leaders. There are also increasing requirements and expectations in terms of responsibility to have an impact on the key environmental and societal challenges. The need for boards and executives to be on top of the context in which they operate will be an essential component of long term sustainable success. Our collective success and sustainability will be linked to solving the three challenges of Decarbonisation and Biodiversity Regeneration, Inclusivity and Fairness, and Digital Privacy and Collective Truth.

“You know capitalism is this wonderful thing that motivates people, it causes wonderful inventions to be done. But in this area of diseases of the world at large, it’s really let us down.” Bill Gates

In my last blog, I tried to emphasize the importance of the role of government in society. Its legitimacy comes from the people; and, to maintain its legitimacy it has to have a clear view of the social contract it needs to deliver against. However, the governments ability to deliver against a credible social contract is underpinned by economic development and growth to drive its financial capacity to provide infrastructure and public services. The main driver of all successful economies has been the market economy and capitalism.

All the strong economies in the world are market economies. The China miracle with a market economy has created consistent high levels of economic growth. It has averaged 9.45% GDP per annum growth rate from 1978 to 2019 driven by the remarkable entrepreneurial spirit and focus on wealth creation of the people. This has been supported by a real commitment to infrastructure development and a strong focus on public services by the government.

A market economy is an economic system in which the decisions regarding investment, production and distribution are guided by the price signals created by the forces of supply and demand. The major characteristic of a market economy is the existence of factor markets that play a dominant role in the allocation of capital and factors of production. Capitalism is a concept integrated with a market economy. It is directed towards making the greatest possible profit for private people and organisations.

Creation of a market economy is one of the key initial roles of a government. There are 7 components to the framework for a market economy.

Profit seeking companies

Free market entry and competition

Strong property rights and enforcement

Absence of central planning, control and price setting

Private ownership of most things

Voluntary exchange

Correction of market failures

Within this framework, there are 5 factors that drive a market economy as shown in Figure 5-1. Firstly on human consumption and wants, Alfred Marshall a leading economist captured the nature of demand, in his 1890 book, Principles of Economics, “Human wants and desires are countless in number and very various in kind….. every step in his progress upwards increases the variety of his needs together with the variety in his methods of satisfying them. He desires not merely large quantities of those things he has been accustomed, but better quality of those things. He desires a greater choice of things, and things that will satisfy new wants growing up in him”

Secondly, technological progress helps address the new and growing desires of a person and where there are new opportunities with customers there are new ways to make more money or openings for new entrants. The profit making goal and opportunity is what drives this technological progress. It helps make products cheaper and better, as well as driving the innovation of new products and services. I will talk in more depth about technology and innovation in my next blog.

Figure 5-1

Thirdly, critical to underpinning the effective operation of a market economy is the efficient movement of capital to where there are opportunities to create value and provide a return to investors. There is clearly significantly more fluidity of finance to opportunities now in the 21st century. Although, the current financial system does have its weaknesses. Returns and rewards are very short term focused and the prime focus of investing and lending is cycling around the financial sector rather than investing in the productive economy. It is estimated that only about one fifth of finance in the US and UK goes into the productive economy. In the S&P 500 today approximately 90% of profits are used for share buybacks and dividends with only 10% invested back in the business. This extractive focus of finance does not help to drive economic growth.

Fourthly on limits to resources, a core part of the effectiveness of a market economy is the efficient movement of factors of production towards producing the most productive goods. The prevailing theory has been that with limits to resources, market driven pricing and the profit motive, these factors help drive the efficient use and allocation of resources. Interestingly, we are now starting to move into a new phase of economic growth that is becoming decoupled from resource use.

Historically, technological progress helped to create more efficient use of resources for any good or service; however, rather than creating a reduced use of resource it resulted in additional consumption in other ways. There was a direct relationship between economic growth and resource consumption. There are now two themes emerging that affect this thinking and the conversation. The first is that we are moving into a world of abundance away from resource scarcity; and the second, is the decoupling of economic growth and resource consumption in developed markets.

Abundance, an idea championed by Peter H. Diamandis a leading thinker on technology and innovation, is the optimistic view that technology and innovation can make rare things plentiful. He cites extensive research where through the use of new technologies costs are dropping 10 to a 1000x based on following innovation curves, such as Moore’s law in the digital space. Energy is becoming more abundant and cheaper as we move to solar and wind technologies. Safe clean water is becoming more plentiful as we are able to desalinate sea water, which is 97.5 of all water, and clean polluted water cost effectively. Food is being produced with less water, less pesticides and less fertiliser. A smart phone is now a communications device that also give you access to the worlds information, books and music. It provides medical diagnostics, it is a camera and video player, a calendar, an atlas and the list goes on. And most importantly it is moving rapidly to be available to everyone.

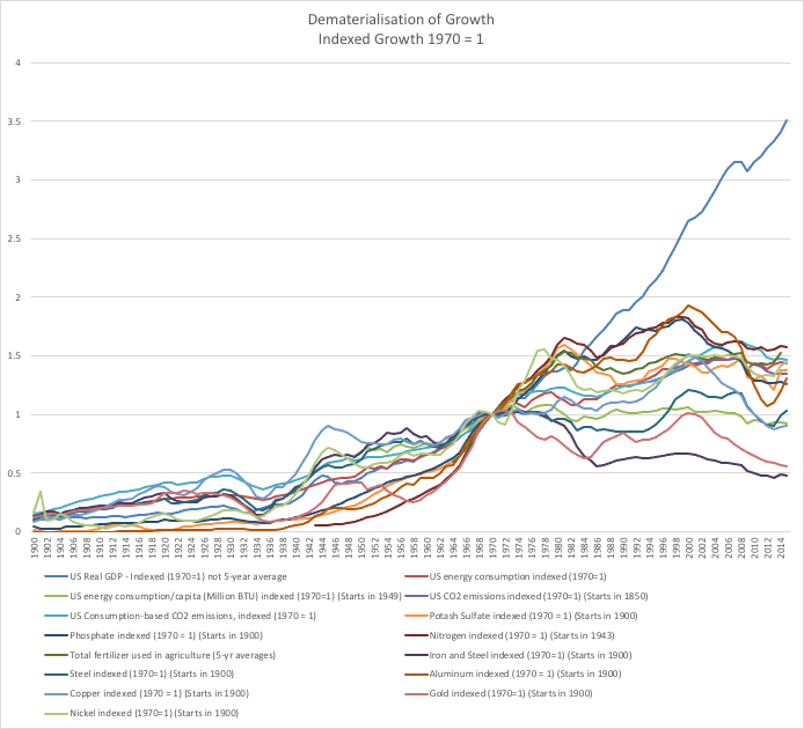

Linked to and associated with how technology is changing how we live, is the emerging net dematerialisation of economic growth. Importantly, it is the combination of technology and capitalism that is driving the continuous movement of creating new and improved goods and services to sell to as many people as possible. So many people believe the world is getting worse because our brains which are survival oriented focus on the negative things. Yet you just have to look at almost any area and the trend lines are improving (See https://ourworldindata.org which was founded by Max Roser, or research by Peter H. Diamandis).

In research conducted by Jesse Ausubel, Iddo Wernick and Paul Waggoner, they did a detailed study of the use of 100 commodities in the US from 1900 to 2010. Ausubel wrote, “…we found 36 have peaked in absolute size…Another 53 commodities have peaked relative to the size of the economy, though not yet absolutely (see Figure 5-2). Most of them now seem poised to fall”. Similar results have been found in research in the UK. This decoupling of material consumption and economic growth is also happening in energy consumption, co2 emissions, farming and water use. This is the power of technological progress and a market economy driven by a profit motive. It is worth reading “More From Less” by Andrew McAfee to learn more about this.

The combination of dematerialisation and abundance should help allay fears of the need to curb economic growth to address climate change. In fact, driving technological progress and economic growth, which go hand in hand, will be critical contributors to addressing the combination of decarbonisation and biodiversity regeneration with inclusivity and fairness globally.

Finally, and contrary to what many people want to think, the government has an important role in the development and maintenance of a market economy. Capitalism alone is insufficient to ensure the well-being of all members and legitimacy of a society. There is a good reason that there is no example of a successful society based solely on capitalism – a model with a sole profit motive cannot stand on its own in building a society.

Material deviations in any of the first 6 components to the framework of a market economy requires the 7th component – correction of market failures by the government. The break down of free market dynamics will inevitably happen without corrections or response. Examples include competitor concentration, restrictions on market entry, use of economic power to control resources, price fixing, imbalances in supply and demand power, taking advantage of factor labour, disregarding consumer safety and security, etc. To date capitalism has not made moral and ethical judgements on what should and should not be done; governments and the law do have the responsibility for these judgements on behalf of society. Capitalism has also not been concerned with inclusivity and fairness which is a fundamental part of the provision of public goods.

It is worth noting that one key area where capitalism does not work is in sectors where there is asymmetry in information and power between the supplier and the customer. A clear example of asymmetry of power is in markets that are monopolistic in structure. Competition laws are designed to help prevent this. As important are markets where there is asymmetry in information, where the value of information is a critical component of decision making. The classic examples of this are in the pharmaceuticals market and consumer financial services. In the pharmaceuticals market, companies are able to egregiously price their drugs to take advantage of consumers who have limited medical knowledge, coupled with health fears, and limited choice because of intellectual property rights. In the financial services’ sector there are too many examples of banks being involved in mis-selling and taking advantage of the complexity of financial products and the difficulty of many consumers in understanding them. Finally, a new emerging area of asymmetry is in digital and social media sectors, where consumers are not able to comprehend the extent to which they are under surveillance and the ways in which their data is being used. This is about the cost of privacy. All sectors where the consumer is seriously disadvantaged as a result of asymmetry need attention in terms of oversight, regulation, legislation, pricing management and consideration of intellectual property rules.

The nature of government involvement in capitalism is important. Reducing the power of capitalism to create economic growth is not in societies interest. Rather it is about harnessing the power of it to drive the overall well-being of society. Governments should be concerned with red tape, and they need to think carefully about the balance of incentives they provide (carrot and stick) and the mix of regulation and legislation. Keeping government interventions as simple as possible, to achieve the desired outcome, requires continuous adjustments.

There is growing thinking that governments need to move more from reacting and responding to market based problems to shaping outcomes proactively. This shaping can be to ensure there is appropriate attention focused on topics such as climate and inequality, to helping the market drive progress in specific areas such as the shift to clean energy and electric mobility. This mission oriented approach can be seen in Denmark and UK with wind power, the US with solar and the development of electric vehicles (and previously the development of the shale energy sector), and Germany with their Energiewende program to transition to a low carbon and nuclear free economy. China has shaped multiple markets linked to their long time horizon plans ranging from the elimination of extreme poverty to being leaders in electric vehicles and wind powered electricity.

At the same time, it is often in industry’s interest to get out ahead of the government and solve problems that if not dealt with will inevitably involve government intervention. We are now starting to see this more actively especially in the areas of waste management and pollution. For example, the Alliance To End Plastic Waste is made up of nearly fifty major global companies. They have committed over $1.0 billion with the goal of investing $1.5 billion over the next five years to develop, deploy, and bring to scale solutions that will minimise and manage plastic waste, and promote post-use solutions. We are also seeing major groups of investors and asset managers driving ESG reporting and starting to allocate their investments aligned to climate and UN sustainable development goals.

The intense focus on pure short term capitalism that has occurred from the 1980’s is starting to shift towards more aligned goals with society, such as climate and inequality, and creating what has to date been defined as ‘compassionate’ or ‘responsible’ capitalism. This will intensify as corporate behaviour is held to account by stakeholder groups and by escalating government agendas on climate, biodiversity, pollution, inequality and the societal impact of technology. It is also being driven at an accelerating rate by investors and asset managers wanting not just ESG reporting but strategies that integrate action on climate and the UN Sustainable Development Goals.

I don’t believe that there is any reason to think that a longer term focused alignment of corporate objectives with those of customers and societies cannot be as profitable as the long term profit outcomes of corporates with their current short term optimization thinking.

In my next blog, I will look more closely at the importance of technological progress and innovation.

#market economy #capitalism #dematerialisation #abundance #free markets #competition #limits to growth #technological progress #ESG #climate change #UN SDGs @Bill Gates @ Peter Diamandis #Alliance to End Plastic Waste

“Take these broken wings and learn to fly”, Paul McCartney

Blog 3 on Post Covid disruption, resilience and innovation.

In the last blog, we talked about changes to consumer behaviour as a result of our current and ongoing Covid experience. Whether we end up living with Covid or are living in a post Covid vaccinated world, consumer behaviour will have changed.

Six areas of likely change were identified, see Figure 3-1 and described in more detail in Blog 2, although the scale of these changes are not clear and will vary across countries and customer segments within a country.

Figure 3-1

The drivers of these changes from the Covid experience to date are:

Structural responses by businesses to Covid. For example, policy shifts by companies towards remote working will make changes to consumer spending and ripple through to the retail and service sector around offices.

Structural responses by governments. For example, rules and regulations on crowds and distancing, or adjustments related to public transport and other types of infrastructure.

Behavioural changes linked to actual and perceived health risks of consumers

Behavioural changes linked to economic changes and uncertainties to large sets of consumers

Changes in the attitudes of sets of people with respect to buying locally as a response to seeing local economic distress in combination with a sense of social responsibility and increased climate change concerns

Responses by the government to address potential future health challenges and alleviate the economic recession we have entered. As an example, this would include accelerated investment in moving a country towards ‘greening’ the economy and society.

The increased rate of change of adoption of existing technology applications and introduction of new technology applications

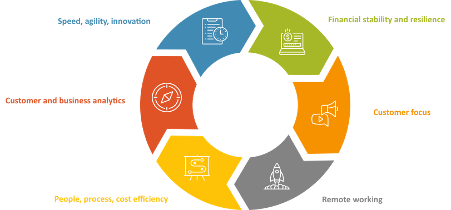

For business, to continue to deal with the Covid crisis, emerge stronger and be on top of these changes there are 6 aspects to running a business that should be top of mind (Figure 3-2). These components are valid for both consumer and B2B businesses.

Figure 3-2

Before we explore the six areas, it is vital that a company does not lose sight of its strategy and what it is trying to accomplish. In my previous series of business strategy, I introduced what I believe is the right strategic framework for the future (Figure 3-3). Having a business purpose that is focused on delivering both a return to investors and a combination of economic, social and environmental impact, is what captures hearts and minds. Engaging the hearts and minds of employees, participants in your supply chain and customers contributes to higher levels of performance and resilience in challenging times. A strategy is also a guiding light around which the changes you need to make and initiatives you need to deliver sit. You want to build a strong business for the medium-long term not just survive the short term!

Figure 3-3

Let’s now explore each of the six activities to help identify opportunities to move forward more effectively. Six months into Covid and I am sure that many businesses are well on the way to making changes and adjusting to a ‘new normal’. I hope some of these factors will add to your plans.

Starting withfinancial stability and resilience, there are 3 areas of particular focus that I want to address (Figure 3-4).

Figure 3-4

Cash is king – For companies that have real concerns about survival, the most important first thing to do is to switch from a prime focus on profitability to a core focus on cash. This combines the focus on revenue and costs with the timing of receipts and payments. Structurally changing the amount of working capital needed in the business can often free up the cash needed to get through difficult times. It also helps a company look in more detail on the specifics of what they are spending their money on, making better decisions on the amount and timing of product purchases for inventory, and the need for new assets and how they might be paid for, such as a rent or a lease vs. outright purchase.

The classic approach to this is to do a 13 week rolling cashflow plus 9 rolling months (12 months in total). To get really focused and extract the most value from this approach the cashflow should be updated on a weekly basis or at least every 2 weeks.

Finance for resilience – If your cash position is not strong and you cannot cover the business challenges through an extended period of time then finding new financing should be a priority. Although in general equity is preferable to debt in times of high uncertainty, if debt is the only answer then you should be looking at increasing your cash position to give plenty of headroom. Remember a bird in the hand is worth more than two in the bush. Banks are notorious for lending you an umbrella when it is sunny and taking it away when it starts to rain; so, be very focused on both the terms of repayment and any covenants on the debt. Before locking in any agreements, be sure there is understanding on the implications of what has been agreed against different challenging scenarios.

If equity is an option, then in general raise a large amount so that there is headroom for a long time and you can ride through potential challenging fundraising times at a later date. It will also allow you to rapidly take advantage of future challenges your competitors may have or aggressively pursue new opportunities. Having too much cash on the balance sheet in the current times is a high class problem!

Scenario Plan – In these times of pandemic disruption, we are now in a non-linear period of change. Extrapolating historic revenue trends is an insufficient approach to financial planning. Building alternative scenarios is the only way. Scenarios should particularly focus on identifying where you might hit critical performance/survival points and what contingency plans need to be in place and triggered as you move towards these points. Creating scenarios over a broad range of outcomes is an essential part of being able to rapidly react to different performance paths, because time is money.

Customer focus is the next area to look at (Figure 3-5) as having a clear approach for efficiently optimising your revenues and contribution is mission critical.

Figure 3-5

Customers First – If the company has been suffering during the pandemic and the challenge is to get back towards old levels of revenues as soon as possible then getting the most cost efficient approach to recovering revenues is what you are trying to accomplish. The simple way to think of customers is that there are three core categorisations to think about – customers, dormant customers and prospects. Customers are those that you currently consider to be ongoing customers and would often be defined as having done business with in the last 12 months. Dormant customers are those that were former customers but are now inactive; consistent with the definition above of customers, these would be customers who have been inactive for at least 12 months. Prospects are potential customers you have never done business with before.

The economics of revenue generation are very different by each of the groups with existing customers being by far the best economically and prospects being the worst. It is true to say that the best way to grow revenues is by first optimising the retention and growth of existing customers. Having to replace customers to stand still is not efficient. Mass product marketing, and not using customer data, will tend to be far less efficient for many businesses.

The likely customer response rates to sales and marketing initiatives are driven by 6 core variables to start with (Figure 3-6). As a company builds experience with targeting, modelling response rates and measuring real results, there should be continuous refinement of the variables.

Figure 3-6

Recency, frequency and monetary value (RFM) looks at the currency and loyalty of a customer. A recent high volume and long term high value customer is the most likely customer to buy from you. For high value – high potential response customers you should be willing to invest more to get them to buy product. For example, you may do a telephone call to high value customers; but, it would be prohibitively expensive to cold call low value dormant customers.

For marketing specific products, you also want to consider channel affinity, timing and product affinity. Channel affinity is the channels of communication and sales channels that have worked in the past with a specific customer. Timing is critical to consider as for example, a product may be seasonal or have specific renewal timing (eg. insurance products). Product affinity is the definition of how close the product you are trying to sell is to historic products that the customer has bought. The closer the affinity, the higher the likely response rates.

For both existing customers and dormant customers personalisation of messaging, offers and promotions will drive up response rates. To drive up the sales value of customers from previous levels you ideally want to know what ‘share of wallet’ you have vs. their full potential with you. This can also be done by evaluating whether low value customers ‘look alike’ with some high value spenders. If you have emails for all customers, subject to GDRP restrictions, then this is an essential low cost communications channel for both existing customers and dormant customers; however, this does not necessarily mean that you should not spend some money to engage in additional ways with high value customers.

For new customers, or prospects, different sales and marketing activities are required. The choice of approach should be linked to the historic cost of customer acquisition and subsequent customer profitability of different sets of activities. It may well be that mass marketing is more efficient than specific targeted marketing at specific prospect segments. If you are doing targeted marketing, then it is valuable to try and profile the characteristics of potential new customers vs. the characteristics of current high value customers (‘look alike’ modelling).

If you have been doing this for some time, with well structured test and control techniques, then you should already be well down the road to efficiently rebuilding your revenues.

Reward Loyalty – In this context, this is about looking for ways to lock in revenue streams for an extended period of time and/or generate pre-purchase revenues to enhance the cashflow and the amount and reliability of future revenue streams. This is effectively looking at alternative business models that will improve your cashflows. You can look at Blog 9 in my Business Strategy series to look at this in more depth. One example of this would be to provide discounts/benefits for minimum levels of pre-payment for future purchases. For example, the Starbucks card generates upfront cash for subsequent use by customers. An alternative example would be to convert an upfront payment to a locked in minimum period of monthly payments. A final example would be to offer a full year’s subscription to a service at a discounted upfront payment vs. the sum of 12 monthly payments. These all can drive improved and/or more reliable cashflows and potentially improve customer retention rates and average revenues per customer.

Listen to Customers – When your business is going non-linear through dramatic shifts in consumer behaviour change – buying habits, use of on-line, and a changing mix of how your customers are spending – then in depth listening to customers on a continuous basis is essential to be able to catch and react to changes as soon as possible. You should use a combination of surveys and in depth discussions to really understand what is driving the changes. The conversations will help you to frame potential changes/solutions to these behavioural changes as well as making your communications more contextually relevant and effective.

Innovate to Retain – With large consumer behavioural changes, more marketing and better messaging alone will not be enough. To retain and grow revenues, innovation across a number of dimensions may well be necessary – channels to market, pricing, packaging, product, services and promotion. Fast effective innovation needs time and attention, robust testing and evaluation, and resource commitment; it should not be an add on to teams that already have a full workload. If you need new skills sets that are not available internally, outsource to make sure that you start well down the experience curve; this is especially important if for the first time you are moving to on-line selling and marketing.

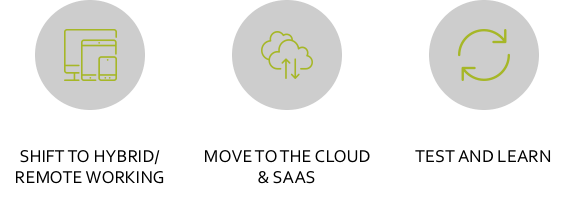

Remote workingis a vital capability for flexibility and to be able to always operate. The pandemic has highlighted this. No company can afford to be without this capability. I have identified 3 key areas to highlight (Figure 3-7).

Figure 3-7

Shift to Hybrid/Remote Working – Remote or hybrid working is not new. Since the beginning of the digital era, the shift started with sales teams, outsourcing services and online selling. Many companies realised that if you move to flexible workspace and allowed some remote work that you only need about 65% of the desks and generate huge savings on office space. The pandemic has made companies realise that remote working is also a resilience capability.

The pandemic has also helped companies test which activities work effectively remotely and which ones don’t. In general, it seems that all types of creative work can be much more effective in person and socialisation between people is an integral part of building effective working relationships. Of course, from a human perspective there are lots of other dimensions that need to be evaluated from the convenience and saving of commuting time, to the inherent need of all of us for socialisation and to the higher challenges of the lower income employees who have less space at home to be able to have a productive working space.

If employees need to work from home then the company needs to ensure that they are equipped to do so with mobile phone, portable computers and screens, adequate internet etc. and, if necessary, adequate space to work. Behind these capabilities for individuals is often the need for a set of team based tools that share calendars, improve productivity and communications, track output and ensure security of data. Solving the ecosystem of how the business works effectively remotely is critical.

Move to the Cloud and SAAS – The cloud and SAAS (software a a service) are great enablers for businesses today. They are the core enablers of enterprise wide hybrid and remote working. You can reduce the need for large tech teams to run your IT infrastructure and variabilise your costs and as we well as adding remote capabilities. Why not allow experts at storage and retrieval, and experts with intensive sector wide applications worry about the applications for non differentiating parts of your businesss in a way that you could not afford to do.

Almost all large companies, that have not already switched, will have a ‘not invented here’ issue with their tech teams and be defending their realm. In a few cases, their in-house systems may drive competitive advantages; but, in most cases it is the fear of change and the idea of technical debt arresting progress rather than the potential benefits of new applications. Do you really think that internally you can build a better cloud at a lower full cost than Amazon, Microsoft, Google and IBM? And, do you think that you can build a better set of customer facing application than Salesforce.com for example? Have a look at their development budgets that you are competing against. Many of these cloud and SAAS applications have already built integrations between them, so the prime focus of attention is the setup, and in some cases customisation, of the solutions to get the full business benefits.

Test and Learn – Going remote may sound easy and it’s just about technology; however, this is all about trying the create the right set up to optimise the interaction of people within the business and with other key third parties. The goal should be to create a new level of performance and not just replicate the in-office approach to work. The measures of success aren’t just on short term performance and productivity measures, the new way of working must also outperform in attracting and retaining the best employees. The company needs to test and learn to find the right people processes and the right tools. The processes need to include the right daily interactions, both task and social oriented, and involve the right tools (eg. Slack) for communicating and interacting.

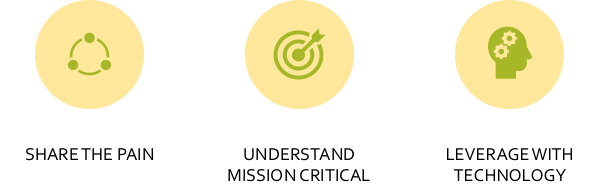

People, process, and cost efficiency need close scrutiny when a business takes a revenue hit and the dynamics of doing business change. It is essential to see how to offset the revenue hit and shift to the right capabilities going forward. Figure 3-8 identifies three areas to cover off.

Figure 3-8

It is easy to ‘slash and burn’ costs and forget about everything else if you are in fear of failing; however, it is useful to be clear on why the company was successful up to the time of the pandemic. Inevitably, it included a combination of the people, the culture and the processes, among other things, that got you there. Don’t forget, it is many of the current components that will also help you to rebound. I also encourage you to consider how to minimise the social cost you may generate by how you address the short term challenges. We all need to face up to the economic, social and environmental challenges around us and do our part.

Share the Pain – Philosophically and practically, each company lives within an ecosystem. That ecosystem involves the company, and all the parts within that organism, and all the other interrelated companies in the supply chain and support sectors. At the extreme for example, if you are running a ‘just in time’ manufacturing operation, then you are completely reliant on the supply side from raw materials to components moving through the supply chain to time; and, if anything disrupts this timing then your business suffers. Against this context of an ecosystem, then any cost reduction activities needs to also consider the implications across the performance of the ecosystem.

When you are looking at cost reduction opportunities, you need to look at all the places that costs can either be taken out, reduced or renegotiated. Depending on how you approach this you can win or lose friends in this process. Maintaining trust, respect and loyalty from those in the business and those you do business with is a key part of the decision making. This is where ‘sharing the pain’ comes in. If people see that the pain is being shared and thoughtfully distributed rather than inflicted on an easy victim you will often be better off. The ruthless exercise of power over a weaker but important supplier does not translate to long term loyalty and reliability; however, displaying an understanding of their situation and trying to solve the problem in a constructive way does.

In the same way, with the potentially devastating impact on certain people from the loss of employment, agreeing that everyone will take a short term pay cut to preserve employment and allow the company to rebound more effectively may be a better answer to dismissals. Shared pay cuts should ideally come in the form of higher pay cuts to the higher paid, or at least the executive teams, whose lives are less affected – this is leadership and an understanding of social impact!

Understand Mission Critical – As businesses evolve in good economic times, it is easy to be less focused on understanding the full relationship of incurring additional costs and the related benefits to revenue and profits. There tends to be a growing pool of ‘nice to have’ vs. ‘need to have’ activities.

In challenging times, getting back to the basics is essential. Start by being very clear on what is critical to attracting and retaining customers, and ideally growing the revenue per customer. With this in mind, then the best way to do this, with the least negative impact, is through process mapping to simplify, speed up, reduce waste, reduce process breakdowns and cut costs. This is the constructive approach to cost cutting.

Leverage with Technology – Across all processes, it is worth looking at where technology could fit and what SAAS (software as a service) applications could be used. The goal is to explore reductions in time, improvements in quality, and reductions in human involvement. There is every reason to believe that there are opportunities in all functional areas. They can range from scanning invoices and automating entry into accounting systems, chatbots and customer self service opportunities, tools for customer relationship management and automated marketing, project management software, HR applications, etc. Many people will be surprised at the extent of opportunities to automate and improve processes with technology.

Customer and business analyticsare most valuable in times of change. They should be embedded in how a company works. There is a lot of talk about KPI’s, balanced scorecards and customer analytics; however, too many companies fall short of what is really required. Every year, the ability to generate or collect information so that a business can be run on facts improves. The faster you receive information the faster you can make informed decisions. There are four key topics (Figure 3-9) to cover off that really make the difference.

Figure 3-9

KPI Driven – Over time I have seen too many companies at the executive level over focus on financial based data; yet, the financial data is the outcome of customer, operational, process, and HR based activities. To take decisions, key information needs to be linked to the root cause of what needs to be managed. Building effective dashboards is not easy but it is invaluable. Cascading down KPI’s is what helps create the linkages between decisions at the top and impact at the coal face.

Continuous Market Analysis – In challenging and uncertain times, being on top of shifts in consumption and customer behaviour and then being able to react is essential. Being able to discern seasonal variations and general volatility from new trends in consumption is the critical skill. This is often helped by active discussions and feedback from customers and prospects.

Integrate with Rapid Decision Cycles – Analysis without consequent decision making has little value. As an example, in the retail fashion sector in the early 1990s many product and sourcing decisions were made typically at least 12 months before the start of the season. Then Gap innovated to move to 6 week cycles of decision making with the finalising of product and volume decisions much closer to the period; and now, Zara can turn around product within 2 weeks to take advantage of in season trends. This type of capability transforms the performance of a business by ensuring the business is not laden with excess inventory, minimising lost sales by taking advantage of high selling items and adding new high selling product in season. Think about the analogies to this in your business.

Speed, agility and innovation is what underpins a company’s ability to react in difficult times and succeed over time. The four components to examine are set out in Figure 3-10. In technology companies, we continuously witness updates in applications and the developments of whole new versions of software and hardware. With Apple, we are on iPhone 11, Apple Watch Series 6, and the Mac OS Catalina soon to be Big Sur. An ability to continuously raise the bar on what you deliver to customers keeps competitors chasing you rather than the other way round. Businesses in all sectors need these capabilities.

Figure 3-10

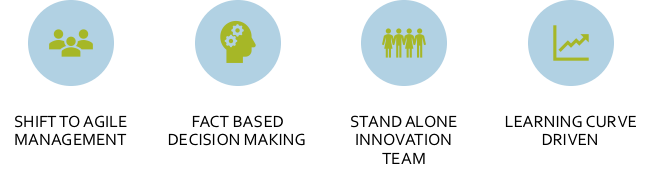

Shift to Agile Management – Agile project management is the most common way that companies undertake software development. It is an iterative development methodology of breaking down development into discrete sets of deliverables, often with a time frame of about 2 weeks, that rapidly speed up development. It also more often than not, does not require the full definition of the end product; rather, that becomes clearer as the team goes through each cycle and incorporates continuous learning related to the end product or service.

The concept of running a whole business also on rapid cycles with clearly defined deliverables is gaining steam. It creates a winning mindset and approach to the business by a management team that is so much more powerful than a standard monthly routine. In some businesses, such as certain retail sectors, it may be better to run on weekly cycles in certain parts of the business.

Fact based decision making – There is no reason to make decisions without facts anymore. That is not to say that you do not also overlay judgements based on analysis of the future. Facts include both internal information and external information (customer, market, competitor, etc.). The critical point to focus on is that agile management requires very current feedback; and in times of great change, such as these, external dynamics can shift very quickly. Just as in retail, you need to be able to identify the hot new products, brands, and shifts in purchasing focus as early as possible. Trying to save money by using less current external information is usually a ‘false economy’.

Stand Alone Innovation Team – In my experience, from running many companies, effective innovation can only be achieved with proper resource dedication and commitment. Without resourcing away from the black hole of day to day management and challenges, the speed of innovation is inevitably compromised. Innovation needs to be seen as mission critical as day to day performance.

Learning Curve Driven – ‘Fail fast’ is the common phrase for companies that are truly learning curve driven. The faster you learn the quicker you can go down the learning curve. This is an essential part of smaller companies outperforming larger slower companies. To effectively learn and push the envelope further and faster culturally, it must be acceptable to fail and not a negative on a person’s performance.

Leadership sits on top of the drive to change, the sets of market initiatives you pursue, and the new capabilities you put in place. The key mindset is to see the unsettling of markets and operations as an opportunity. Leadership needs to think like an attacker not and incumbent. They need to be thinking about new opportunities, new markets, new ways of doing things, new applications of technology and leading with empathy and inclusion. For most people, change is uncomfortable; however, for leadership it needs to become a way of life and a challenge you look forward to conquer.

The next blog, will explore the implications for governments of the post Covid, or living with Covid world.

“You cannot avoid the responsibility of tomorrow by evading it today”, Abraham Lincoln

Blog 15 of the Business Strategy Series

This is the final blog on the strategic framework and of the Business Strategy Series. I will be continuing to write on related subjects. I am also working on another series that will look at the roles and linkages of the market economy and the state – another critical subject as we work through these turbulent and challenging times. A coordinated response between the market economy and governments is mission critical for solving our climate crisis and we can see how vital it is for other disruptions such as the pandemic we have now lived with for 6 months.

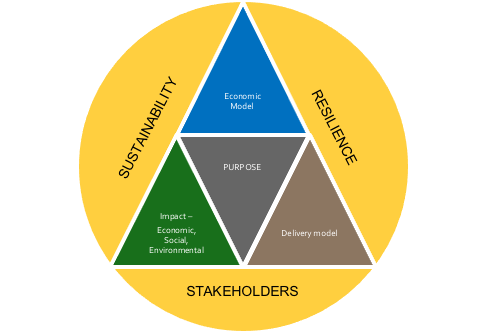

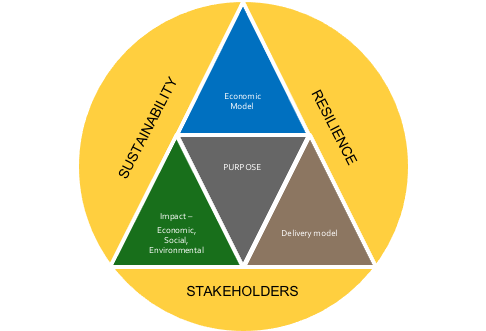

The components in the strategic framework (Figure 15-1) that have been introduced are focused on helping business executives and their boards create a long term sustainable business that has a true purpose in society by delivering both economic returns to investors and impact to other stakeholders.

Figure 15-1

To date we have discussed purpose and the delivery model. In this blog, I want to talk a bit more about impact, strategic timeframes, sustainability and resilience. I will then complete the discussion with a short piece on portfolio strategy.

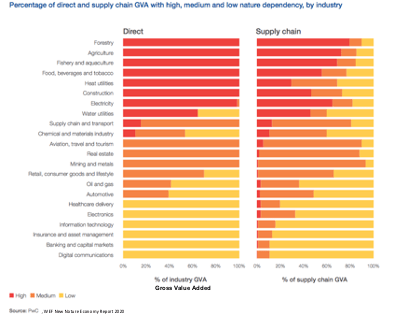

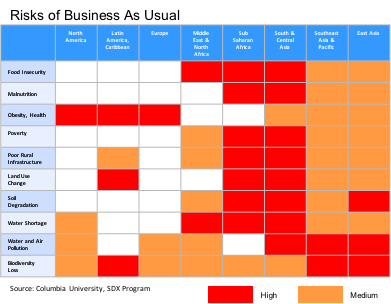

Starting with environmental/climate impact. Through the ESG reporting requirements (Environmental, Social, Governance), companies are being asked to look at the environmental at both level 1 impact, which is the company’s direct impact, and level 3 impact which considers the full supply chain impact including product use. Clearly, at the environmental level the specifics of each sector, and its supply chain, will have different environmental dependencies and different opportunities to create impact. Key sectors such as energy, food, packaging, retail, manufacturing and fashion which have high resource use, significant energy and water usage, and large supply chains will have high environmental impact unless they have already taken action (Figure 15-2). The urgency to create full circular strategies and lead the way is most vital for these high dependency companies; although, that should not stop all companies from moving forward as well.

Figure 15-2

Taking the view at the societal level, that the climate problem can be solved by just focusing on the major companies that are contributing to climate change, reduced bio-diversity, high water use, etc. is definitely insufficient if you look at the science. Part of the solution is for the public to be also looking at their consumption and making it more in tune with the needs for environmental sustainability. So the full and necessary challenge is to create a major shift in how we all live and how businesses, the government and NGOs operate.

As I noted in Blog 14, for companies delaying this shift to a societally responsible strategy will only result in an increasingly challenging shift for each year of delay as the need to hit targets by certain dates will not shift. Each company in each sector needs to set ambitious and timely targets to make its contribution to this. It is management’s, and the Board’s, challenge to ensure that the strategy they set meets both its economic needs and its responsible level of impact.

In addition to the sector, the geographic footprint of a business has implications for the impact focus and targets that it sets (Figure 15-3). For example, companies that have large supply chain footprints in the developing world need to be thinking much harder about its specific social impact goals that it wants to achieve. Truly exploring the UN Sustainable Development Goals will help define these. Business as usual in many parts of the world will perpetuate the fundamental environmental, social and economic challenges that need to be overcome.

Figure 15-3

A helpful approach to thinking about how to incorporate impact programs and goals into the business is to look at the leading companies that are already a long way into this journey to be a responsible company.

One of the companies leading the way is Unilever, who have been focusing on this now for over 10 years. They now report on their progress against their goals each year (Figure 15-4).

From their website, you will see that they have created specific time based targets that roll up to overall ambitious goals, they have linked them to the Sustainable Development Goals, they are tracking their performance over time and they are publishing their performance publicly.

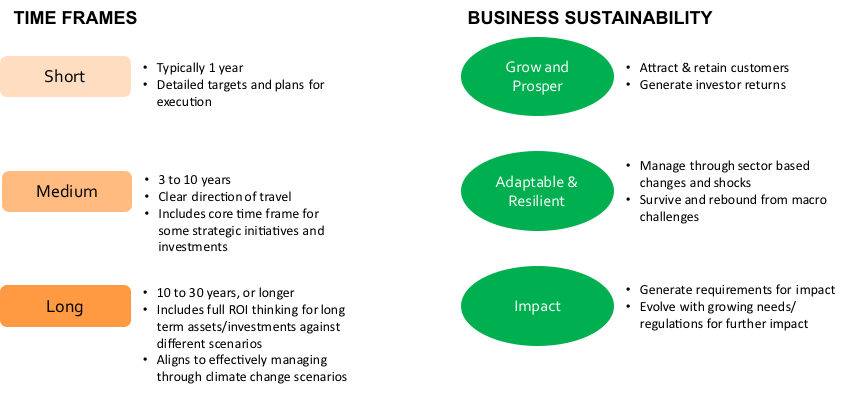

As noted in Blog 12, strategic timeframes need to be extended vs. the typical 3 to 5 year timeframe (Figure 15-5). A longer term time frame needs to be added to consider fundamental impacts such as climate, major changes in technology adoption and putting in place the right components for resilience. 3 to 5 year thinking and short term ROI horizons will not ensure adequate thinking on the sustainability of a strategy.

Figure 15-5

Linked to this, it is critical that there is a proper review of the potential activities and events that change markets and/or generate new opportunities (See Figure 15-6 for examples). These events will range from changing views on environmental responses required, SDG compliance, new regulations, a changing geo-political environment and of course the potential for massive impact from new and converging technologies.

Figure 15-6

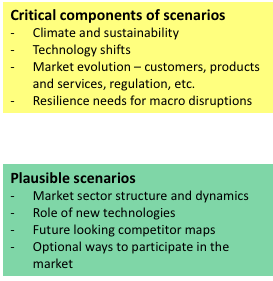

More important than ever is to develop strategic scenarios that would be effective based on different views of what could happen in short, medium and longer term horizons (Figure 15-7). The approach for doing this is to pressure test strategic options against different externalities and come up with some plausible scenarios to evaluate. These scenarios need to be developed holistically and need to be comparable. The components of the scenarios should cover off customers, products/services and supply chains, investment, metrics, people, processes and technology.

Figure 15-7

With a real analysis of alternative scenarios, the comparison should provide further clarity around the performance opportunities for the business as well as the risk parameters. The true strategic options can be explored along the key dimensions of profitability/ROI, impact, implementation risk, meeting of key stakeholder needs, sustainability and resilience.

This moves strategic thinking significantly on from a pure profit and shareholder only focus. In the short run, realigning the business to survive this pandemic and be able to prosper in the post Covid world, having an organisation that is proactively progressing on gender and race issues, as highlighted by the ‘black lives matter’ and ‘me too’ movements, and making a real contribution to the global climate/environmental targets that need to be met are big topics in most board rooms, and with investors, employees and customers. These challenges need much more than tactical reactions, they are strategic and structural challenges that will inevitably require some major changes to most businesses in terms of how they operate, who they do business with, where they invest, and what performance targets can be expected.

The overall strategy and each of the components should fit coherently into the strategic framework (Figure 15-8). Continuous evaluation of the components of the strategy over time and looking for ways to continuously improve and refine the strategy is equally as vital as the initial setting of the strategy. As the rate of change in the world accelerates, dynamically adjusting/refining the strategy and improving execution is mission critical. Speed and agility are much more important than a singled minded short to medium term focus on efficiency.

Figure 15-8

The final subject, I want to touch on is the implications of this in a company with a portfolio of businesses. Investors and stakeholders will be looking at the overall economic and impact performance of the business. Non-performing business units within the portfolio will have an overall effect on the attractiveness of the business to investors, employees and other key stakeholders.

The proposed approach to evaluate a portfolio of businesses is a four step process (Figure 15-9). Firstly, evaluate the portfolio of businesses from an economic perspective. Secondly, overlay the environmental impact of the businesses on to the economic performance of each of the businesses. Thirdly, look at the full alignment of the set of businesses against sustainability impact which will include social and economic impact. Finally, look at the portfolio options from a resilience perspective. This review should be done considering the realistic potential scenarios of each of the businesses.

Figure 15-9

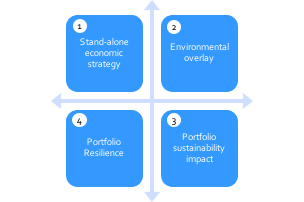

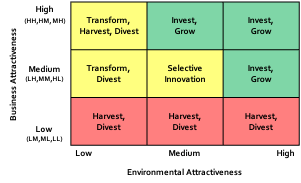

Now looking at each of these components in a little more depth. Starting with the stand-alone economic strategy, we have the traditional grid looking at business position vs market attractiveness (Figure 15-10). Both components of the strategy should be looked at from a short, medium and longterm perspective. Business position is the combination of profitability, market position, and ability to maintain performance over time as markets change and evolve. Market attractiveness is the combination of size, growth and the economic attractiveness of the market. The grid should be fairly self explanatory. If you have a strong market position in an attractive market then you ideally want to stay in the market and should be willing to invest and grow your position. Whereas, if you have a weak position in an unattractive you would rather manage the business for cash or divest from the market and reinvest the capital in more attractive businesses.

Figure 15-10

Moving on to the Environmental overlay (Figure 15-11), this takes the overall position from the economic strategy grid in Figure 15-10, Business Attractiveness, and matches it against the Environmental Attractiveness of the business. High environmental attractiveness has a low or positive environmental footprint within the timeframe of meeting the targets set by the Paris Climate Agreement and the environmental focused SDGs. For many businesses, the key target is the year the company will achieve a Net Zero carbon emissions equivalent level 3 footprint (ie. including the full supply chain of the business).

Overall, unattractive businesses, unless you have clear sight on how to transform them, should be harvested and/or sold. If an unattractive business is also very unattractive from an environmental perspective, such as a coal business, it is more likely that this should be divested as attracting investors and raising funds in your overall business will tend to be more challenging. In an equivalent way, if you have a small business with real potential in an environmentally attractive sector it may well be that you should be diverting your investment capacity into this business to build it. An interesting set of companies to watch on these dimensions will be BP, Shell and Exxon. Both BP and Shell have committed to reach a Net Zero CO2 emission target by 2050. It is not yet clear that they have strategies set out on how to achieve this; but, what is clear is that they will be redirecting their cash generation to the renewables sector where they have much smaller strategic positions. It has been a broad set of stakeholder pressures, including collapsing share prices, that have driven the adoption of these strategic commitments.

Figure 15-11

The third component of a portfolio review is the review of the alignment of impact overall with the business portfolio options (Figure 15-12). Although, climate impact tends to get the lion share of the attention from the press, economic and societal impact are vital components of the SDGs, and in many business and geography combinations, as you can see in Figure 15-3, they may be more important than climate impact. The food sector, including food retailers, are a great example of this with their broad geographically spread supply chains.

Figure 15-12

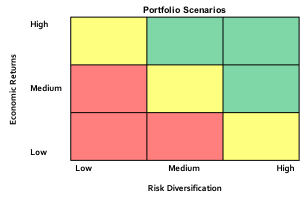

Finally, having evaluated the businesses, and their strategic options, in an overall and comparative context, the final step is to compare realistic combinations of businesses from a portfolio perspective. In particular, given the businesses have been evaluated against the three areas of impact, the portfolio options should be looked at from an economic return vs. a risk diversification perspective (Figure 15-13). The risk assessment is against the longterm sustainability and resilience of the portfolio scenarios. Adjusting a portfolio to reduce risk has real value, as we have seen in this pandemic. The potential benefits of a tight focus of businesses in terms of sector, geography, supply chain, efficiency and commonality of disruption risks may not be justified from a sustainability and resilience perspective. As I have noted before flexibility, adaptability, and diversification can provide real value to the business overall.

Figure 15-13

This brings to a conclusion, the series on Business Strategy. I hope you have found it thought provoking and useful; and hopefully, it will help you make a difference in your business and create a deeper impact in the world around you.

I will continue to write blogs to delve in deeper to sectors and subjects that will explore strategy and sustainability in a deeper context. As noted in the about section of my blog, REBOOT is not just about business, it is about the need for structural changes, or a new operating system, across all areas connected to our lives and our world.

Please continue to follow, share, engage in conversation, contribute and also reach out to me if you want to talk about this further. I can be reached through LinkedIn.

“Without a sense of purpose, no company, either public or private, can achieve its full potential. It will ultimately lose the licence to operate from key stakeholders.” Larry Fink, CEO, Blackrock