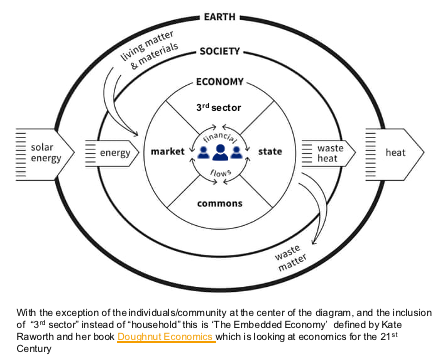

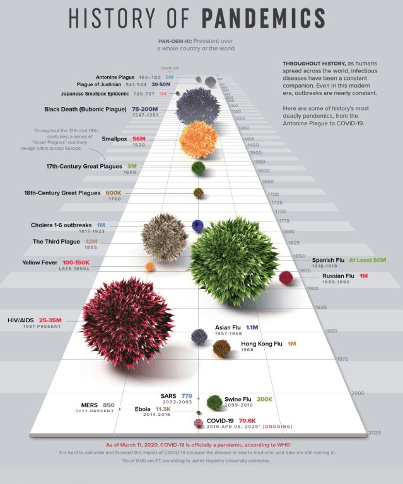

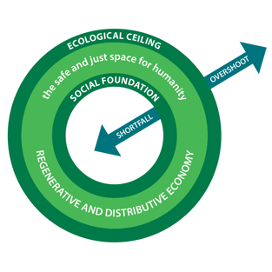

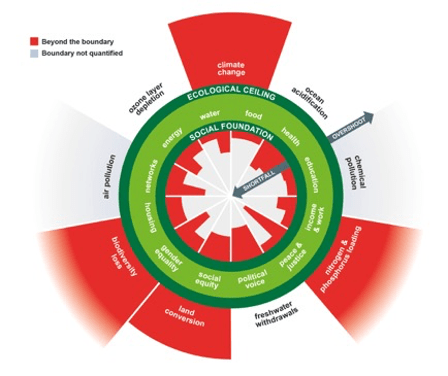

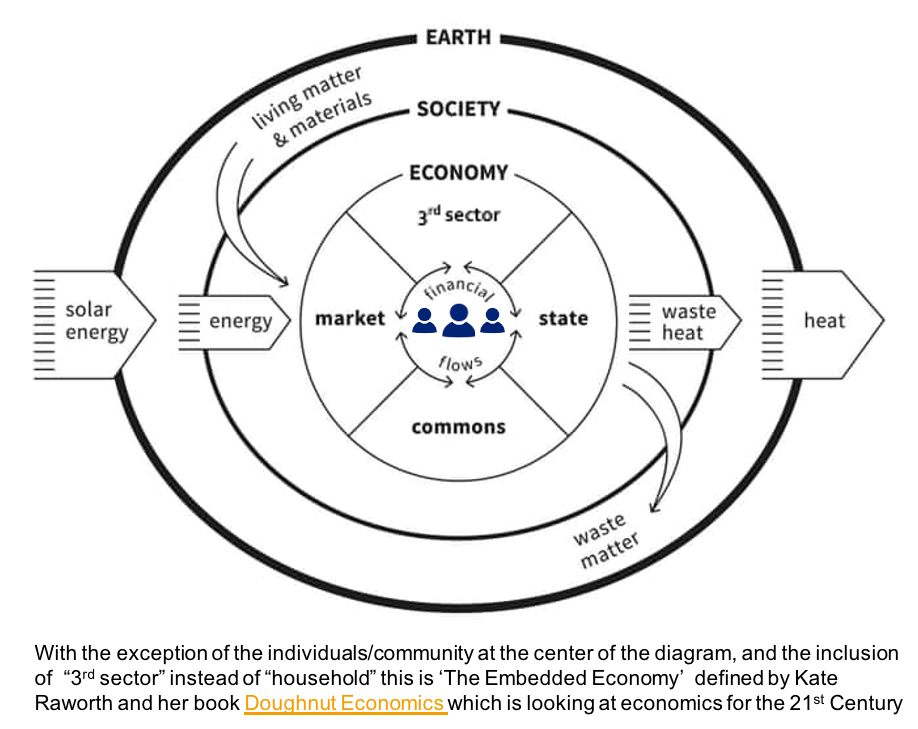

Kate Raworth’s diagram of the Embedded Economy (Figure 3-1), with my adaptation, is a useful framework to think systemically about the global context in which we live and critical interconnections related to our economies, societies and the environment. This model shows the key components of the global system with the individual in the centre, surrounded by the components of the economy, which sits within a society and reside in the global ecosystem. This is not a fully closed system as the earth is fuelled by the sun and it also dissipates heat. There is also consumption of scarce resources by society and generation of waste that goes back into the environment. This is the framework or macro-ecosystem that we need to get in balance to be sustainable.

Our current system is not in balance! In this Anthropocene era, we are increasing the heat of the planet which is affecting the living world. At the same time, we have been changing land use, displacing and causing the extinction of fauna and flora, depleting finite resources and then disposing of waste matter in unecological ways. We have taken the world out of its most stable 12,000 year period, which has been the period of great human development, into an unsustainable cycle.

This model for driving sustainability does not have the state in the centre as in the case of command economies such as Russia and China with individuals as participants in a state led system. It also does not have free markets and capitalism sit in the centre, as it does currently in the Western world with the overwhelming focus on capitalism and corporates, with the individual or citizen secondary. This also is not a plutocracy model, which as Nobel Laureate economist Joseph Stiglitz describes America moving to a government “of the 1%, by the 1% and for the 1%”.

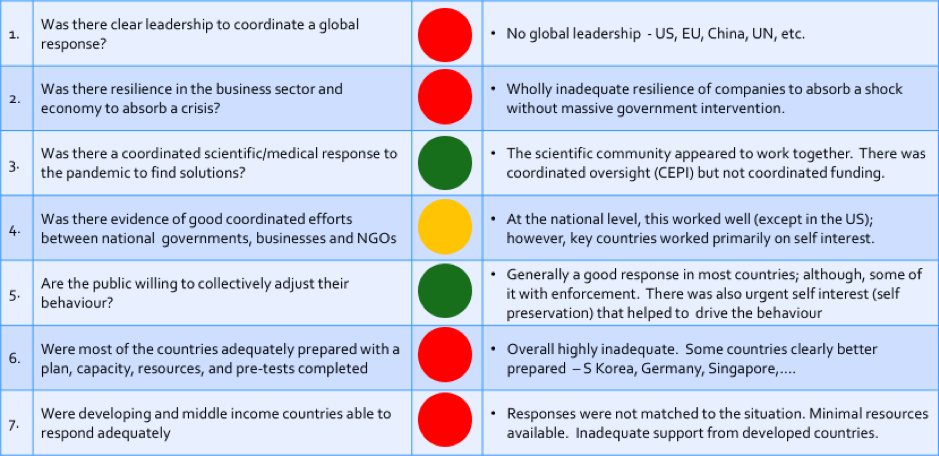

You just have to look at your life to realise that society has not been properly oriented on citizens. There are occasional exceptions, such as war and the current pandemic, with generate some small rebalancing. A perfect example of this corporate centricity is the public bailout of the financial sectors misdemeanours in the 2008 Great Recession.

This lack of primary focus on the individual is apparent in a myriad of ways. The unequal delivery of public services such as health and education to individuals. The reduction of services levels, or raising of prices, when public services are outsourced. The use of public funds to bail out failing corporates and financial institutions. The inadequacy of financial and legal consequences for currency manipulation, interest rate manipulation and mis-selling by financial institutions. The weak governmental response to pollution and environmental damage. The declining levels of personal privacy.

The primacy of the corporation over the individual also manifests itself in what appears to be small ways; but, are cumulatively substantial. We have virtually no control over our personal information on the web. We are served terms by websites in order to use them that are unintelligible, onerous and leave us no choice but to accept. We see subscriptions from companies that cause term based commitments; yet, companies are able to change their terms of the contract throughout the period. With regulated companies, such as telecoms, we see that it easy to sign up to new services on the web, yet it is incredibly difficult to cancel services and it needs to be done through their understaffed call centers. And the list goes on.

Proper protections for consumers would not allow this corporate behaviour, and it would provide material enough penalties to the corporates that they would not repeat offend. The only way to create a sustainable model is to focus how we operate to be citizen centric and not corporate or government centric.

Individuals are consumers, employees, voters, environmental stakeholders and members of communities. If we are to build a better model of how we operate then we need to define what the social contract that societies should be striving to provide. This provides the moral compass for where we are trying to get to. The other components in the society, in particular the state, the market economy and the financial markets need to be aligned and incentivised to deliver against this target social contract.

The target social contract is the “North Star”, it defines that the individual consents to surrender some of their freedoms, participate in and abide by the rules of the society and submit to the authority (in the case of a democracy to the decision of a majority) in exchange for the protection of their remaining rights, personal safety and security, maintenance of social order, access to employment to earn income, and provision and access to public services. The social contract that I am referring to is the set of expectations that a member of a society should be able to have that is consistent with building a strong, fair and sustainable society for future generations.

The rights of an individual start with the UN Declaration of Human Rights that was signed in 1948 and was adopted by a vote of 48 in favour, 0 against and 8 abstentions. Today there are 193 member states of the UN, all of whom have signed on in agreement with the Universal Declaration of Human Rights (UDHR) by signing at least one of the nine binding treaties influenced by the Declaration, with the vast majority ratifying four or more. Currently, 79 of the countries have independent National Human Rights Institutions that comply with International Standards.

The rights include 30 basic human rights. The foundation of the Declaration are the principles of dignity, liberty, equality and brotherhood. Sitting on these principles are the rights of individuals; the rights of the individual in civil and political society; spiritual, public and political freedoms, and social, economic and cultural rights.

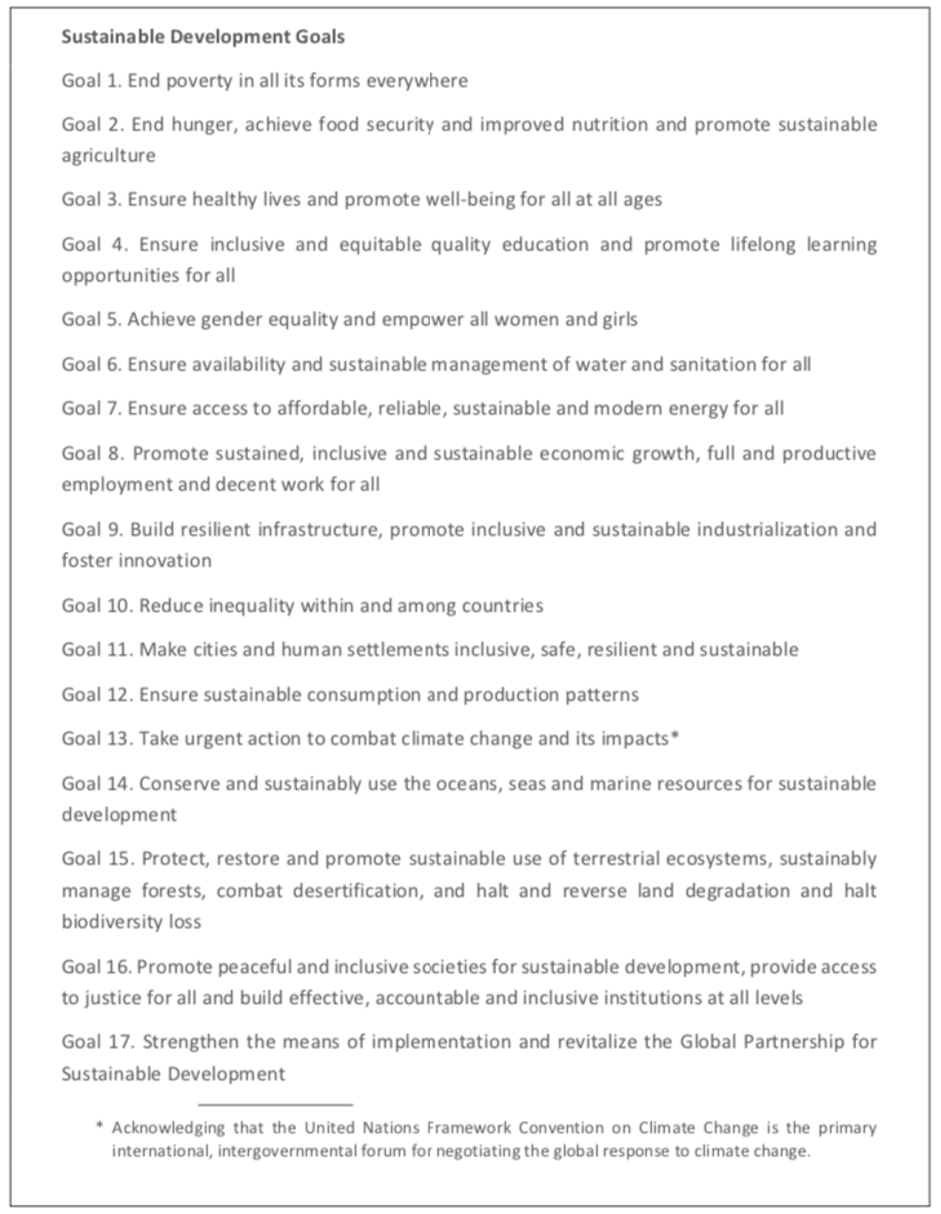

The 17 UN Sustainable Development Goals (SDGs), see Figure 3-2, take these concepts of human rights and add further specificity. Over 90 percent of the goals and targets of the SDGs correspond to human rights obligations. These SDGs defined in 2015 and agreed by over 190 countries, have an agenda and targets set for 2030.

It is important to note that across many of the SDGs is the key phrase “for all”. This is a big shift in thinking on what is expected from a society and how the thinking behind the delivery of services is changing. The shift has been from average and median thinking to heterogeneous thinking and focus on the importance of inclusivity, or the elimination of exclusion, and overall fairness. A. Philip Randolph captured this when he said, “A community is democratic only when the humblest and weakest person can enjoy the high civil, economic, and social rights that the biggest and most powerful possess”. It is the focus on ensuring that the world we live in is less plutocratic.

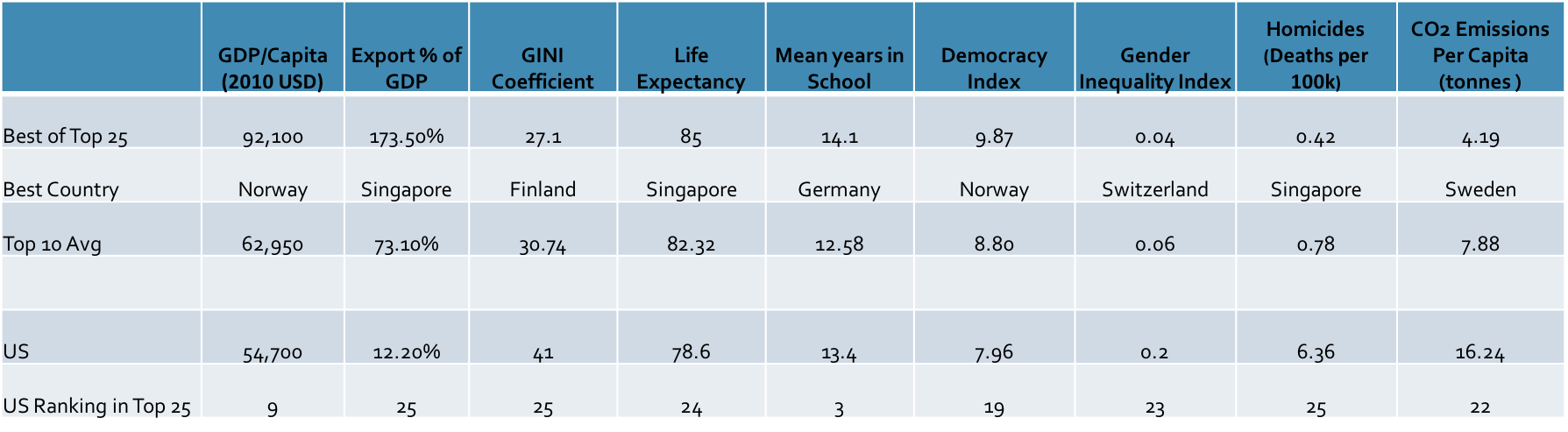

Inclusivity and fairness thinking is not socialist thinking and does not exclude wide ranges of income between people. It does contemplate that everyone has some minimal rights and a right to fair treatment. SDG’s are not the enemy of capitalism; rather they are foundations of compassionate and responsible capitalism which in the medium and longterm will be dramatically more sustainable than short term zero-sum-gain thinking. As I showed in my previous blog, the most prosperous countries are also the most well balanced. Fair compensation, high levels of employment, good health, education and strong social security have multiplier effects on the prosperity of a society.

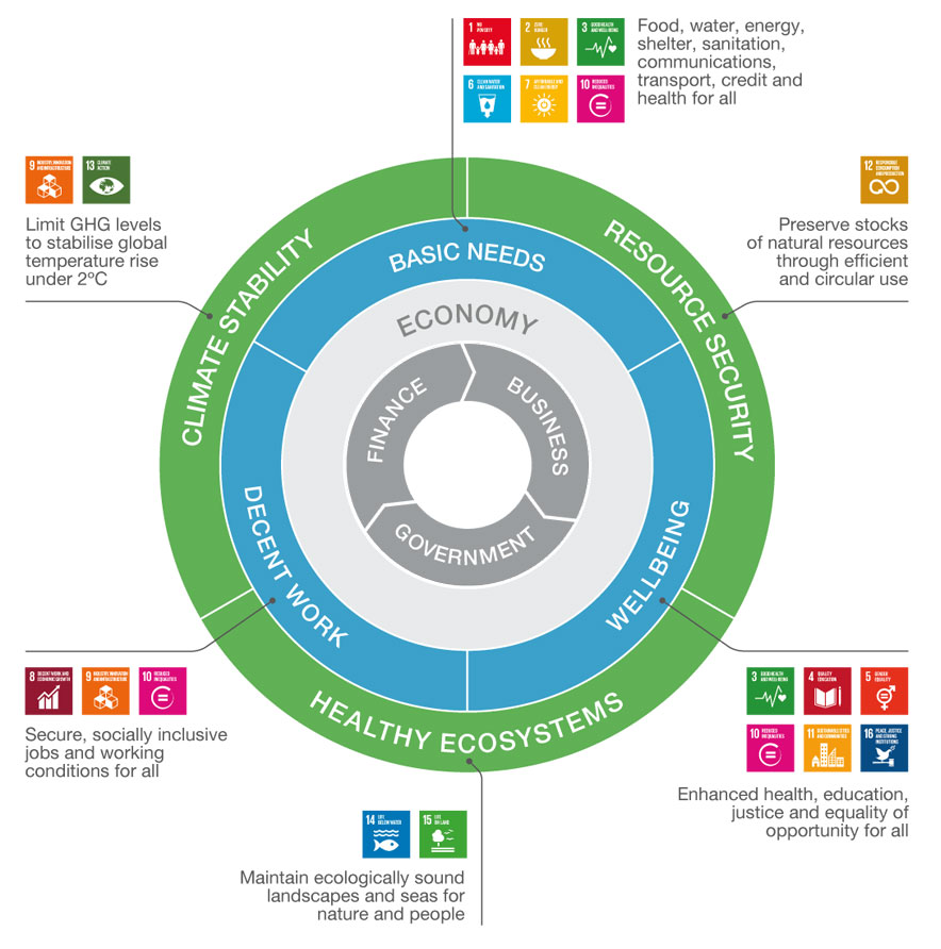

The Cambridge Institute for Sustainable Leadership, has linked the SDGs into three broad social ambitions and three environmental ambitions (Figure 3-3). These social ambitions revolve around basic needs, decent work and wellbeing.

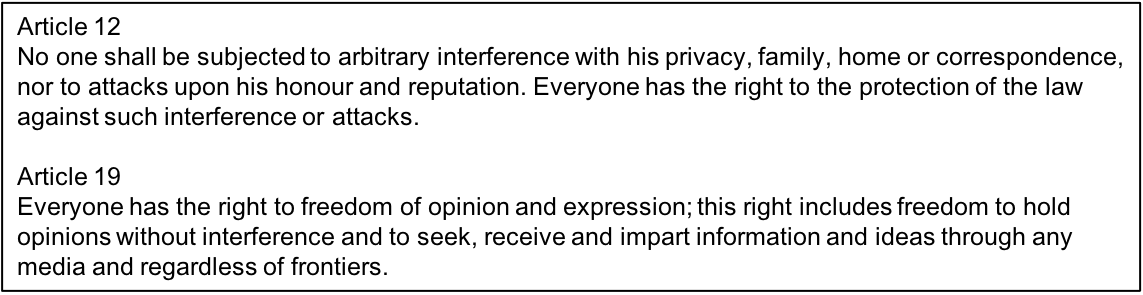

These three needs are vital components of the target social contract; but, there are also additional components required. The pervasive digital gathering and use of data attacks privacy. This capability combined with the proliferation of communications and the ability to personalise and deliver fake news to mislead, misinform and misdirect behaviour is a real societal problem. These real and tangible issues relate to Articles 12 and 19 defined in the 1948 Declaration of Human Rights (Figure 3-4).

At the time these were written it would not have been possible to predict the impact of technology. As I noted in my first blog of this series, even now it is almost unfathomable how much data on each person is being gathered and how it is being used. This along with the personalised delivery of communications which can be either true or fake news is creating real cracks in societies. The 2016 and 2020 US presidential elections have provided a real magnification of what can happen. How can a country become so polarised and how can 70% of the Republican voters truly believe there has been massive fraud no matter what the courts say or even what the people who have managed the elections say? The answer is that the information they watch, read and have been fed is different. In democratic countries with only mass media, it used to be that the truth would rise to the top and there would be a common set of information. In most countries, there were also rules on the accuracy and balance of information that was provided to voters to help them make their decisions. False information was filtered out by reputable media and there were rules on the truth of advertising messages. Social media has bypassed this with the ability to push personalised communications that can be either true or fake, and algorithms that reinforce the personalised messages, so there is no longer a common set of facts that all people will see. Is it possible to maintain an effective and stable democracy without a common set of information and facts from which citizens cast their votes?

There is also a fundamental bias of information driven by both mass media and social media. We are increasingly seeing that the public view of what is happening in the world is severely distorted from reality. Figure 3-5 illustrates this distortion perfectly. If this is the case on a subject such as causes of death, imagine the levels of distortion of reality of other relevant topics to the individual. If we believe that transparency, data and facts, and truth is paramount to the individual who is a consumer, an employee, a voter and a member of a society, then this is a fundamental social contract issue that must be solved.

Inevitably the ability to increasingly personalise can be both positive and negative. Providing more relevant information or advertising more relevant products and services for consumption can have real value to the individual. However, having information on race, gender, sexual orientation, disability, health, income, etc. can also allow for discriminatory behaviour and pricing for exclusion or to take advantage of an individuals circumstances. With increasing use of AI, which relies on historical data this can help to reinforce old practices. We have seen an example of this in 2018 when Amazon was innocently trying to make their recruitment more efficient and found that because of historical data they continued to reinforce gender bias. The more disturbing use of data is when it provides a company asymmetric knowledge vs. the consumer and they then exploit this opportunity. Asymmetry of knowledge and power has been an age old problem with financial and pharmaceutical companies exploiting their situation making customer the big losers. This problem now has arguably crossed the line with how social media companies and other tech giants exploit consumers and their data to enhance their business and keep out competition. The collection of data is continuing to gather steam and will explode further with the penetration of IoT based devices and the growing levels of information from biotech and neurotech applications. Privacy control must be one of the fundamental rights of an individual going forward.

We are seeing the progressive escalation of concern on the power of the large tech companies, in particular the GAFA group – Google, Apple, Facebook and Amazon – with respect to both privacy, anti-trust and misinformation. The GAFA have between them faced anti-trust challenges and investigations in multiple regions including the US, EU (including individual countries within the EU), India, Canada, Australia, and Japan. Even though fines have been in the billions of dollars this is pocket change for these companies. The focus on getting the tech giants under control will only escalate.

Meanwhile some progress has been made with the GDPR (General Data Protection Regulations) that went into effect in May 2018 in the EU and is helping to set the standards that other countries will move towards. The GDPR regulations do have some privacy related rights related to data deletion, previously known as “the right to be forgotten”; but, this is incomplete. This may be a big step for corporations; but, it is only a small step from an individual’s perspective on rights to privacy.

So, to conclude there are five categories of components of a social contract to create an individual and citizen centric society that can thrive and prosper going forward. As identified above by the SDGs and CISL, there are the three requirements of basic needs, well-being and decent work. The basic needs involve minimum levels of availability and access to food, water, shelter, energy, sanitation, communications, credit and transport for all. It is vital to note that availability and access also included fair pricing. In terms of wellbeing, there is affordable healthcare and education, and equal access to justice, safety and security. Healthcare needs to be comprehensive and should not result in gaps as big as 10 years expected length of life differences at birth depending on which side of the street you were born. The nature of access to education, is about narrowing the gap to affordable and high quality education to provide life and mobility opportunities. This education includes K to 12, University and apprentice/applied educational programs and reskilling. The third requirement is decent work. Decent work comprises living wages, social security programs to assist in managing through out different work situations, being disabled and pension arrangements. Access to ongoing education to provide mobility will be increasingly important as the fourth industrial revolution, particularly with respect to AI and robotics, becomes increasingly pervasive.

Wrapping these three requirements is the fourth component, which is the right to be living in a climate and environmentally sustainable environment. The climate and environmental challenges are both global and local issues. Due to the climate urgency and the potential implications of missing the Paris Climate Agreement target of not more than 2 degrees Celsius increase in average temperature, overall this is the most important component of the social contract. We know we are tracking to hit over a 3 degree increase in temperature. This has critical consequences for different countries including liveability, the local economy, access to food and water, and massive inter-country issues such as environmental refugees. Environmental refugees are also inevitably linked into both economic and political refugees. The refugees crisis can only increase from its current estimated level of 80 million of which 46 million are internally displaced people according to UNHCR. Predictions of 200m or more climate migrants by 2050 are not uncommon. The ripple effects of this should not be underestimated in terms of human cost, economic cost, rising populism and societal destabilisation.

The fifth component comprises the core human rights of privacy, access to facts and the truth, and the interlinked rights of freedom of information and freedom of speech. At the heart of privacy is personal control over all the personal information that is gathered, generated and used in the public arena of the internet and other networks of information. Collective access to data, information and the truth has to be essential. This means that fake news needs to be clearly identified, be managed in its distribution, and restricted in critical areas such as advertising and the social media push of content. Social interaction and discourse needs to have common ground based on truth for societies to operate effectively. Finally, freedom of access to information and freedom of speech is fundamental. The debate around this is rightly growing and becoming increasingly complex with developing factors such as the growth of ‘fake news’, the social media driven and algorithmic based delivery of content, the emerging “cancel culture”, and the growing voice of a full range of minority interests.

Being definitive on the requirements of each of the components of a “North Star’ social contract is complex; but, excusing ourselves and not progressing on them is irresponsible. Each country will need to define their specifics behind a common set of principles for all countries. The vital thing is that we become individual and inclusive centric to how we ‘reboot’ to create more sustainable societies and a more sustainable collective world.

At the heart, the social contract is about solving inclusivity and fairness, which is the solution to the problem of inequality. We can see the urgency to address the growing issue of inequality in many countries. Yet in context, Branko Milanovic, an expert on global inequality, assesses that about 80% of inequality is across countries as opposed to within countries (Branko Milanovic, “Global Inequality – A New Approach For The Age of Globalisation”). Solving multi-lateral problems is exponentially more complex than country problems. I will explore this and inequality in more detail in later blogs.

In my next blog, I will looking in more detail at the role of the government in a democratic society.

#social contract #climate change #global warming #Universal Declaration of Human Rights #inequality #inclusivity #fairness #privacy #digital trust #cyber #mass manipulation #truth #Global Inequality #SDGs #Sustainable Development Goals #Paris Climate Agreement #UNHCR #UDHR #refugees @Kate Raworth @ Joseph Stiglitz @Branko Milanovic @CISL @Google @Apple @Facebook @Amazon